In China, the preferential individual income tax (IIT) policy which has been applicable for one-off annual bonus payments from 1 January 2019, was set to expire on 31 December 2021. At the weekly State Council executive meeting, which was held on 29 December 2021, Premier Li Keqiang made the announcement that the preferential tax policy for annual bonus payments will be extended to the end of 2023.

Send us your question and we will answer within 24 hours. Message →

What Does this Mean?

Effectively this means that the bonus policy as per Cai Shui (2018) No. 164 (hereafter referred to as Circular 164), will continue to be applicable until 31 December 2023.

As per Circular 164, tax residents in China who receive one-off annual bonuses will have their bonus payments calculated independently from their comprehensive yearly income. The taxation of the annual bonus separately from a tax resident’s comprehensive income generally allows for a lower tax rate to be applied, depending on how an individual’s income has been structured.

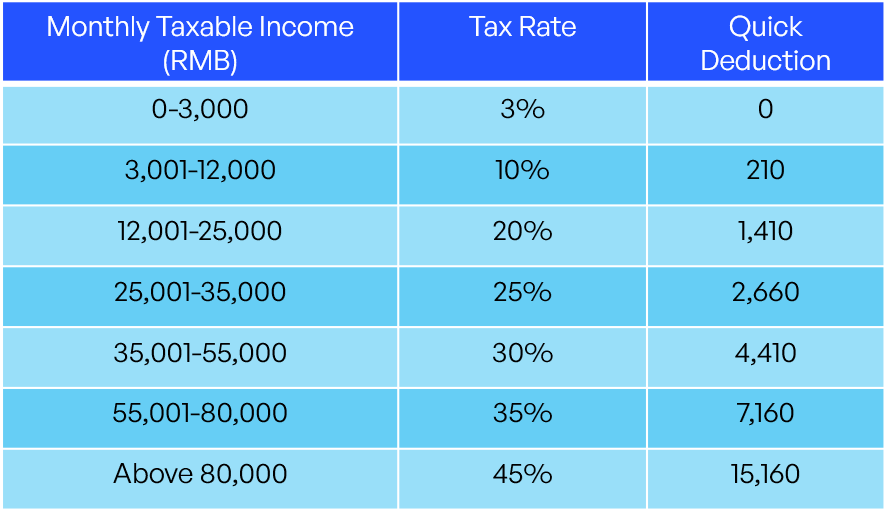

An annual bonus can be calculated according to the following method:

- IIT on annual bonus: (Taxable income from bonus*applicable tax rate) – quick deduction.

- Taxable income from bonus = annual bonus/12

The corresponding tax rate can then be found in the table below:

For example, the amount of IIT due on an annual bonus of RMB 50,000 paid to an employee in Shanghai would be:

- Taxable income from bonus: RMB 50,000 / 12 = 4,166.67

- IIT on annual bonus: (RMB 50,000* 10%) – RMB 210 = RMB 4,790

- Net bonus received by employee: RMB 50,000 – RMB 4,790 = RMB 45,210

If the policy had not been extended, tax residents would then have their one-off annual bonus payments combined with their comprehensive yearly income and thereafter calculate their IIT.

Who Qualifies as a Tax Resident?

As per IIT legislation in China, an individual is considered a tax resident if the individual has resided in the country for 183 days or more in a calendar year. An individual who has resided for less than 183 days in a calendar year is considered a non-resident.

Why has the Policy Been Extended?

According to the State Administration of Taxation, the policy has been extended in an effort to reduce the burden of personal income tax and alleviate the pressure felt by lower- and middle-income groups.

Find Out More About the Tax System in China

For both employers and employees, it is important to understand the complexities of the Chinese tax system, to better manage financial resources as well as take advantage of the benefits available. Learn more in our article A Complete Overview of the Tax System in China, to stay better informed of how the tax system in China works.

How We Can Help Your Business in China

For more than a decade MS Advisory has been assisting SME’s across China and Hong Kong with all their accounting, financial advisory and business setup needs. We are dedicated to delivering high quality through transparency, compliance, and attention to detail. Get in touch with us today and let our consultants provide you with the understanding you need to enhance your operation in China.